Revision of Interest Rates for DBS Multiplier, BOC SmartSaver and UOB One Account from 1 August 2020

By The Boy Who Procrastinates - July 31, 2020

With the interest rate cut by US Fed, the era of high-interest yielding savings accounts is coming to an end. With effect from 1 August 2020, 3 more financial institutions will be revising the interest rates of their savings accounts, namely the DBS Multiplier, BOC Smartsaver and UOB One Account.

This article aims to provide an overview of the upcoming changes, how the existing account holders may be affected by the revision and to reveal which are the banks that still offer the best interest rate.

Revision of Interest Rates for DBS Multiplier Account

Starting from August, DBS will be implementing changes in 2 main areas. First, the scope of dividend crediting will be expanded as follows:

Instead of confining to SGX, the eligible sources of dividends will include all markets via DBS Vickers. Furthermore, dividends from DBS Unit Trust and DBS Invest-Saver will count towards the total amount of eligible transactions under the Income category.

On the receiving end, dividends credited into SRS and CPFIS accounts will be regarded as qualifying transactions. However, it should be noted that dividend crediting still comes under the Income group and does not constitute a separate category on its own.

On the receiving end, dividends credited into SRS and CPFIS accounts will be regarded as qualifying transactions. However, it should be noted that dividend crediting still comes under the Income group and does not constitute a separate category on its own.

With that, I reckon that the impact from this revision would be minimal unless you have been receiving significant amount of dividends from DBS Unit Trust, DBS Invest-Saver or overseas stocks via DBS Vickers, or into your SRS account and CPFIA, which may bump up to the next transaction bracket.

In any case, this alteration definitely offers greater flexibility around the definition of dividend crediting.

Now, the unpleasant news is that DBS will be reducing the interest rates for the fulfillment of Income criterion and transactions in 1 and 2 additional categories.

For Income + transaction in 1 category, the reduction in interest rate appears to be uniform across the transaction brackets with a decline of 0.70 percentage point.

For an average account holder who has been relying on the combination of salary crediting and credit card spend with transaction amount in the range of $2,500 and $5,000, he will be earning just 0.9% interest rate from August onwards, down from the current 1.6%.

For Income + transaction in 2 categories, the reduction in interest rate is less pronounced, ranging from 0.40 to 0.70 percentage point.

To earn greater interest and higher balance cap, existing account holders may be incentivised to attain transactions in more categories besides Income. I have briefly discussed about some strategies that an account holder can employ to achieve transactions in 2 categories.

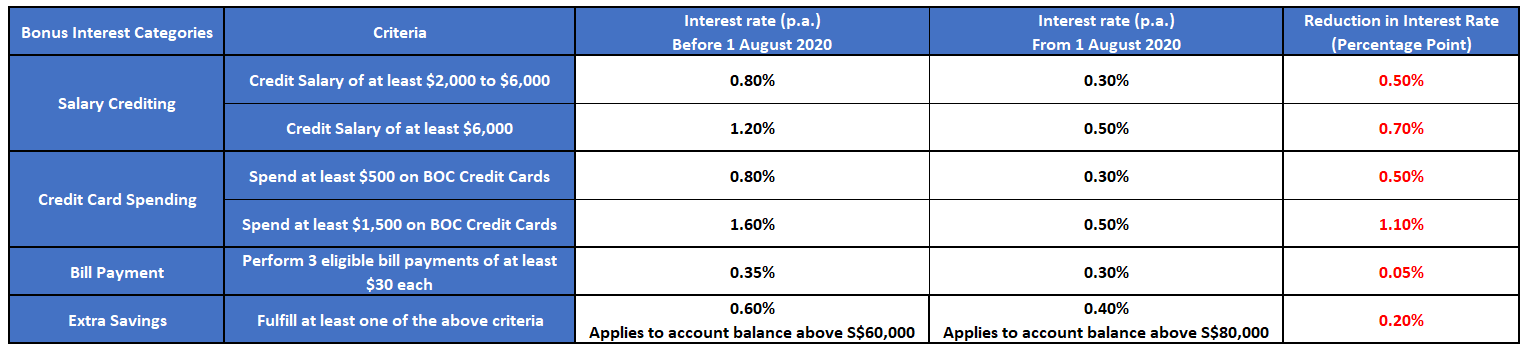

Revision of Interest Rates for BOC SmartSaver

From August onwards, BOC SmartSaver will be revising the prevailing interest rate which is tiered based on the amount of account balance.

Across the tranches, the reduction in base interest rate ranges from 0.175 to 0.275 percentage point. Account holders will be earning 0.1% for balance up to $20,000 and 0.15% for balance up to $100,000.

Across the tranches, the reduction in base interest rate ranges from 0.175 to 0.275 percentage point. Account holders will be earning 0.1% for balance up to $20,000 and 0.15% for balance up to $100,000.

On top of that, the bonus interest section will undergo major reduction as follows:

There will be a decline of at least 0.5 percentage point for the bonus interest related to salary crediting and credit card spending. The bill payment category is the least impacted with just a decrease of 0.05 percentage point.The Extra Savings bonus interest will apply to account balance above $80,000 instead of $60,000 from August.

A new category that awards bonus interest for the purchase of eligible BOC wealth product has been added but there seems to be limited information surrounding this category. Given that the BOC website has listed RMB funds, insurance and unit trust as part of the wealth products, I would assume that it is one of these 3 options.

For an account holder who credits his salary, spends on his BOC credit card and pays 3 bills, he will be earning 0.9% bonus interest, down from the current 1.95%.

Overall, the revised interest rate chart, inclusive of the prevailing interest rate will be as follows:

The bonus and prevailing interest rate remains largely within the range of 1% to 1.04%. Subsequently, it climbs to 1.12% from $80,000 onwards due to the boost from extra savings category. However, it should be noted that this would require a significant capital of $100,000.

On top of that, the bonus interest section will undergo major reduction as follows:

There will be a decline of at least 0.5 percentage point for the bonus interest related to salary crediting and credit card spending. The bill payment category is the least impacted with just a decrease of 0.05 percentage point.The Extra Savings bonus interest will apply to account balance above $80,000 instead of $60,000 from August.

A new category that awards bonus interest for the purchase of eligible BOC wealth product has been added but there seems to be limited information surrounding this category. Given that the BOC website has listed RMB funds, insurance and unit trust as part of the wealth products, I would assume that it is one of these 3 options.

For an account holder who credits his salary, spends on his BOC credit card and pays 3 bills, he will be earning 0.9% bonus interest, down from the current 1.95%.

Overall, the revised interest rate chart, inclusive of the prevailing interest rate will be as follows:

The bonus and prevailing interest rate remains largely within the range of 1% to 1.04%. Subsequently, it climbs to 1.12% from $80,000 onwards due to the boost from extra savings category. However, it should be noted that this would require a significant capital of $100,000.

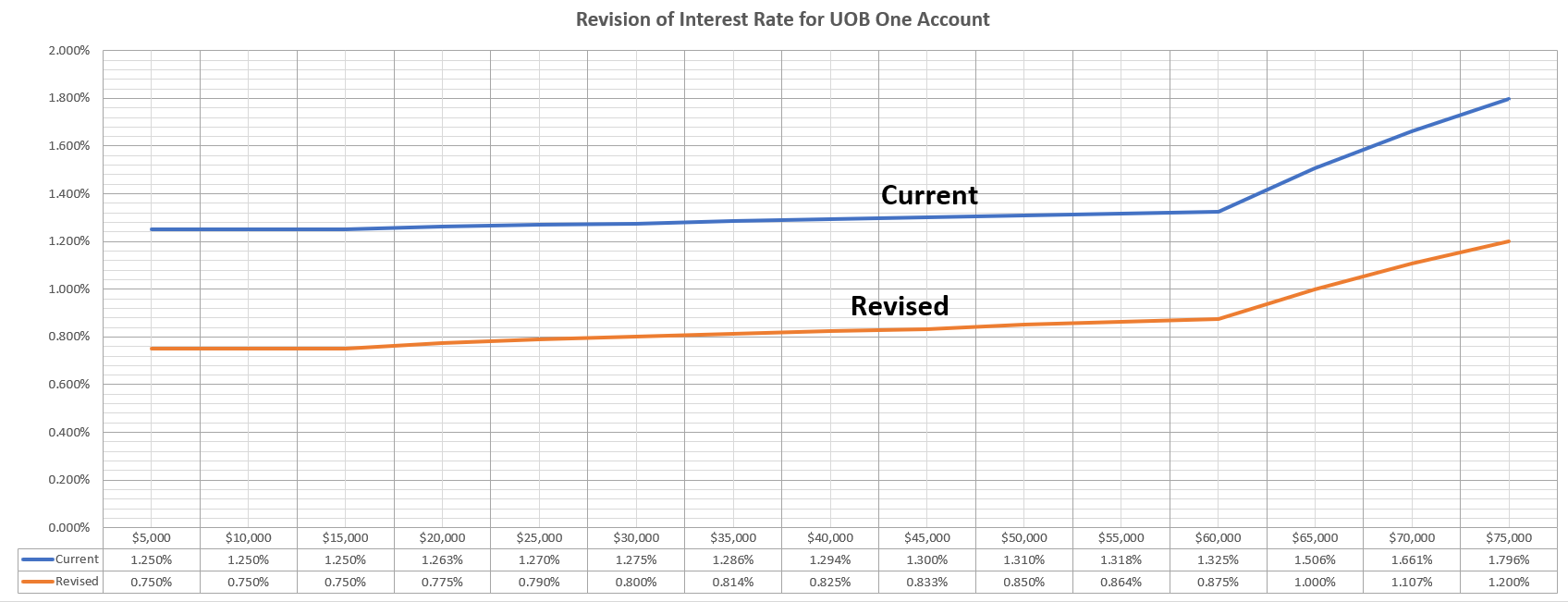

Revision of Interest Rates for UOB One Account

From 1 August, the interest rate for UOB One Account will be reduced across each balance tranche of $15,000 as shown in the table above.

The impact from the revision is the most pronounced after the first $60,000 balance in which bonus interest rate will be reduced by 1.18 percentage point!

The impact from the revision is the most pronounced after the first $60,000 balance in which bonus interest rate will be reduced by 1.18 percentage point!

With the first $75,000 balance, an account holder will now be earning the revised interest rate of 1.2%, a decline of approximately 0.6 percentage point. That translates to a loss of $38 interest per month.

Overall, the decrease across the account balance varies between 0.45% to 0.6%.

Overall, the decrease across the account balance varies between 0.45% to 0.6%.

Overview of the Interest Rates for the 3 Local Banks

This chart may be useful for those who are only interested in savings accounts offered by the local banks. It is unsurprising that the Aug revision by DBS and UOB will see better alignment of interest rates among the trio.

For the first $50,000, the fulfillment of Income and 2 categories for DBS offers the highest interest rate at 1.5%. For a larger capital at $75,000, UOB One Account still maintain its competitive edge at 1.2% despite the revision.

Comparison with other Active Savings Accounts

When set side by side with other active savings accounts, we can see that these banks are now offering similar interest rates in response to the interest rate cut by US Fed.

In this current low interest rate environment, the UOB One Account and OCBC 360 Account offer the best bang for the buck at 1.2% effective interest rate. Even with the revision, BOC SmartSaver is still offering a decent 1.12%, but it comes at a considerable capital of $100,000.

Comparison with other Savings Instruments

Running the risk of having an over-simplistic comparison, I have picked a few other conservative financial products to have a general idea of the yields across various instruments. These are alternate avenues to earn interest without exposing to significant risk.

- Singapore Savings Bonds: Using the data of the Aug 20 issue, the interest rate for first year is a pittance of 0.27%. The minimum investment amount is $500 for each issue.

- Fixed Deposits: If you do not mind forgoing liquidity, DBS currently provides the highest interest rate of 1.15% on a 12-months fixed deposit with a minimum placement of $1,000.

- Citi MaxiGain Account: Taking 1-month SIBOR to be at 0.25, the base interest is calculated to be 0.125%. The bonus interest can reach a maximum of 0.6% after 12 months of stepping up. Hence, the total interest rate sums up to be 0.73%.

- CIMB FastSaver Account: A fuss-free savings account that offers competitive interest rate of 0.825% on the first $100,000 balance which can be an attractive alternative to active savings accounts.

- RHB High-Yield Savings Account: Another fuss-free savings account that is similar to CIMB FastSaver Account. Account holders can earn 0.08% on the first $10,000 and 1% on the next $90,000. The effective interest rate is calculated to be 0.908%.

- Singlife Account: Instead of a savings account, the Singlife Account is basically an insurance savings plan that delivers 2.5% p.a. returns on the first $10,000 and 1% on the next $90,000 with no lock-in period. The returns are calculated daily and credited on a monthly basis. It should be noted that the capital in the Singlife Account is protected under the Policy Owners' Protection Scheme (PPF Scheme) by Singapore Deposit Insurance Corporation (SDIC) but the interest rates of 2.5% and 1% are not guaranteed.

- Stashaway Simple: This cash management portfolio invests equally in the LionGlobal SGD Money Market Fund and LionGlobal SGD Enhanced Liquidity Fund, both are funds that invest in short-term debt instruments. While the net returns is projected to be 1.9% with no minimum balance, investors should be informed that the returns is not guaranteed and may fluctuate in volatile economic conditions. As with other investment products, it is not totally risk free and there is possibility, albeit remote, of losses. Furthermore, the invested capital is not insured by SDIC.

- ABF Singapore Bond Index Fund: The ETF invests in the constituents of the iBoxx ABF Singapore Bond Index which tracks a basket of high-quality bonds issued primarily by the Singapore government and quasi-Singapore government entities. Based on its declared 2020 dividend of $0.0249 and the recent price of $1.264 (as of 30 July), the dividend yield is approximately 2%. Kindly note that this is excluding any capital gain/loss due to price movement on the bourse.

If there has been a large pile of idle cash sitting around, one may consider turning to invest for the long term after setting aside the required portion for emergency.

If you do not wish to miss out on any articles, you may consider following the facebook page for timely update.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institutions and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institutions and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

2 comments

Thanks for sharing the blog, seems to be interesting and informative too. Can you suggest some of the interesting places to visit for investment linked insurance

ReplyDeletehttps://saglamproxy.com

ReplyDeletemetin2 proxy

proxy satın al

knight online proxy

mobil proxy satın al

YRE