Revision of Interest Rates for OCBC 360 Account from 1 July 2020

By The Boy Who Procrastinates - June 27, 2020

Before the OCBC 360 Account is able to cement its place as one of the highest yielding savings instruments, OCBC has announced another round of interest rate revision for this prized savings account that will take effect from 1 July 2020. You may also wish to refer to the OCBC notice for more information.

This article aims to provide an overview of the upcoming alteration, how the existing account holders may be affected by the revision and to find out where else to park your funds so as to ensure that they are still working hard for you.

Revision of Interest Rates for OCBC 360 Account from 1 July

A 180 degree reversal from the upward adjustment in May, OCBC will be halving the interest rate awarded for salary crediting as above. Furthermore, bonus interest related to credit card spending will no longer be offered from 1 July. The Save Bonus (achieved through monthly incremental average daily balance) will remain unchanged at 0.2% and 0.4% for the first and next $35,000 respectively.

Based solely on these 2 categories, the effective interest rate for $70,000 balance will be reduced significantly from 2.4% to 1.2%. And this comes with the challenge of sustaining the Save Bonus in which there are 4 methods that I have outlined in the previous post.

In my opinion, this upcoming revision will deliver the final stroke as the interest rate offered by the OCBC 360 Account will be lower than its peers. In addition, the paltry rewards hardly commensurate with the effort needed to maintain the Save Bonus requirements.

OCBC has cited "weakened interest rate environment" and "challenging macro climate" for the motivation of interest rate reduction. Hence, the implementation of interest rate cuts by other financial institutions may well be undertaken in the near future.

Overview of the Revision of Interest Rates for the 3 Local Banks

(Click to enlarge)

With the upcoming revision for OCBC, the updated interest rates trend lines for the 3 local banks, in balance increment of $5,000, are shown in the chart above.

The OCBC 360 Account has lost its competitive edge with the upcoming revision, offering lower interest rate than UOB One Account. For sizable balance amount above $30,000, the UOB One Account offers a decent interest rate in the range of 1.275% to 1.8%.

Despite the recent revision, DBS Multiplier Account is still able to maintain its allure as a flexible savings account that mostly caters to lower account balance in the range of $25,000. Setting up a Regular Savings Plan can be a viable option to attain transactions in other categories and optimise the additional interest.

Despite the recent revision, DBS Multiplier Account is still able to maintain its allure as a flexible savings account that mostly caters to lower account balance in the range of $25,000. Setting up a Regular Savings Plan can be a viable option to attain transactions in other categories and optimise the additional interest.

If you just want a savings account to credit salary...

For those who are earning sufficient salary to split into two savings accounts or just prefer to earn bonus interest for salary crediting, this comparison may be of interest.

(Click to enlarge)

The DBS Multiplier has remained as one of the favourite choices with its flexibility around the credit card spending requirement. As long as a monthly salary of at least $2,500 is credited, account holders can choose to spend a minimum of $1 on the DBS/POSB Credit Card to obtain 1.6% interest.

Even after the revision, OCBC 360 Account will still be offering 0.9% interest rate on the crediting of salary of at least $1,800.

Even after the revision, OCBC 360 Account will still be offering 0.9% interest rate on the crediting of salary of at least $1,800.

The BOC SmartSaver offers 0.8% bonus interest for salary crediting of at least $2,000. On top of that, it allocates different base interest rate based on the account balance tier. Therefore, the total interest rate would be slightly higher than what was illustrated above.

The UOB One Account was excluded for comparison as credit card spending forms the primary prerequisite for bonus interest.

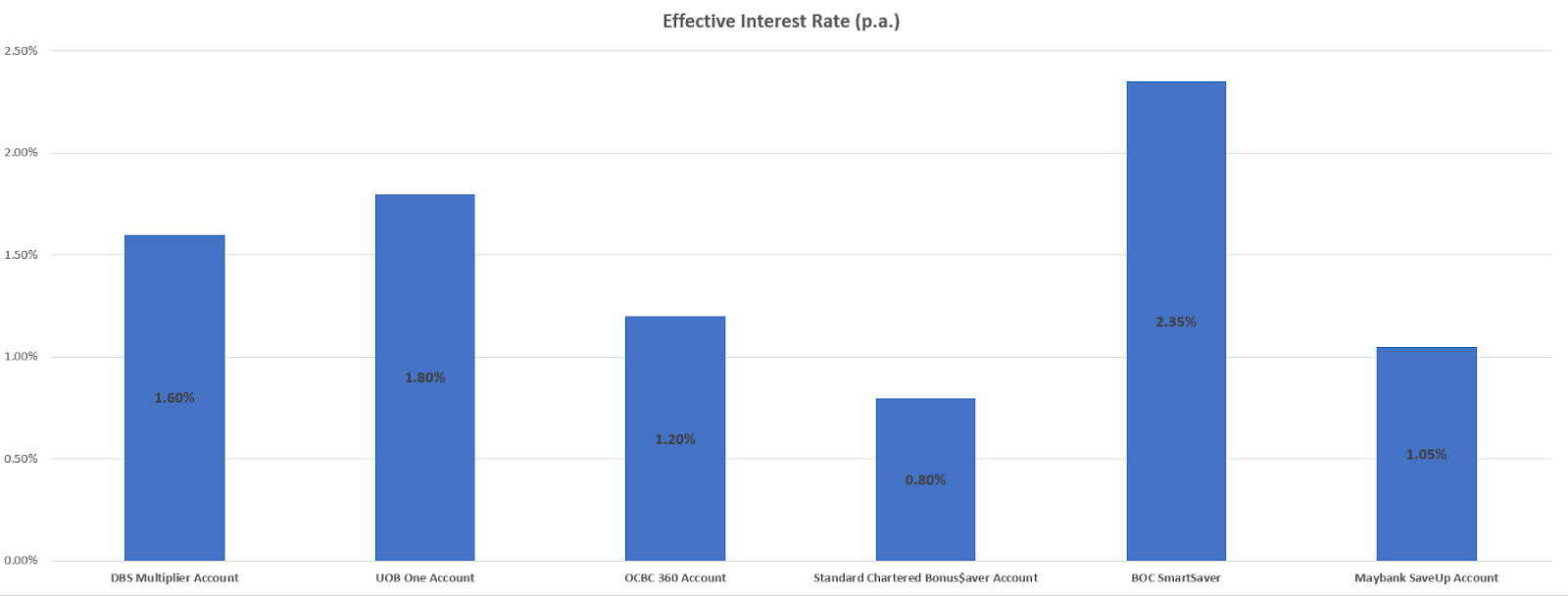

Comparison with other Active Savings Accounts

(Click to enlarge)

When set side by side with other active savings accounts, the effective interest rate offered by the revised OCBC 360 Account has paled in comparison considerably.

At this point, the BOC SmartSaver offers the best bang for the buck at 2.35% effective interest rate. UOB One Account is still offering a decent 1.8% even after the recent change in May.

At this point, the BOC SmartSaver offers the best bang for the buck at 2.35% effective interest rate. UOB One Account is still offering a decent 1.8% even after the recent change in May.

Before scurrying to set up new savings accounts with the higher interest rate, one should be mindful that impending interest rate cuts by banks might be inevitable with the low interest rate environment.

Comparison with other Savings Instruments

Running the risk of having an over-simplistic comparison, I have picked a few other conservative financial products to have a general idea of the yields across various instruments. These are alternate avenues to earn interest without exposing to significant risk.

(Click to enlarge)

- Singapore Savings Bonds: Using the data of the July 20 issue, the interest rate for first 2 years is a pittance of 0.30%. The minimum investment amount is $500 for each issue.

- Fixed Deposits: If you do not mind forgoing liquidity, Maybank currently provides the highest interest rate of 1.30% on a 24-months fixed deposit with a minimum placement of $25,000. For a shorter period of 12 months, DBS is offering 1.15% with a minimum placement of $1,000.

- Citi MaxiGain Account: Taking 1-month SIBOR to be at 0.251, the base interest is calculated to be 0.126%. The bonus interest can reach a maximum of 0.6% after 12 months of stepping up. Hence, the total interest rate sums up to be 0.73%.

- CIMB FastSaver Account: A fuss-free savings account that offers competitive interest rate on the first $100,000 balance which can be an attractive alternative to active savings accounts. The upcoming revision from 15 July will see its interest rate lowered to 0.825%.

- RHB High-Yield Savings Account: Another fuss-free savings account that is similar to CIMB FastSaver Account, RHB will be revising its interest rate with effect from 1 July. Account holders can earn 0.08% on the first $10,000 and 1% on the next $90,000. The effective interest rate is calculated to be 0.908%.

- Singlife Account: Instead of a savings account, the Singlife Account is basically an insurance savings plan that delivers 2.5% p.a. returns on the first $10,000 and 1% on the next $90,000 with no lock-in period. The returns are calculated daily and credited on a monthly basis. It should be noted that the capital in the Singlife Account is protected under the Policy Owners' Protection Scheme (PPF Scheme) by Singapore Deposit Insurance Corporation (SDIC) but the interest rates of 2.5% and 1% are not guaranteed.

- Stashaway Simple: This cash management portfolio invests equally in the LionGlobal SGD Money Market Fund and LionGlobal SGD Enhanced Liquidity Fund, both are funds that invest in short-term debt instruments. While the net returns is projected to be 1.9% with no minimum balance, investors should be informed that the returns is not guaranteed and may fluctuate in volatile economic conditions. As with other investment products, it is not totally risk free and there is possibility, albeit remote, of losses. Furthermore, the invested capital is not insured by SDIC.

- ABF Singapore Bond Index Fund: The ETF invests in the constituents of the iBoxx ABF Singapore Bond Index which tracks a basket of high-quality bonds issued primarily by the Singapore government and quasi-Singapore government entities. Based on its declared 2020 dividend of $0.0249 and the recent price of $1.244 (as of 26 June), the dividend yield is approximately 2%. Kindly note that this is excluding any capital gain/loss due to price movement on the bourse.

If you do not wish to miss out on any articles, you may consider following the facebook page for timely update.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institution and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

1 comments

https://saglamproxy.com

ReplyDeletemetin2 proxy

proxy satın al

knight online proxy

mobil proxy satın al

A6KQQA