Revision of Interest Rates for DBS Multiplier, OCBC 360 and UOB One Account from 1 May 2020

By The Boy Who Procrastinates - April 24, 2020

With the interest rate cut by US Fed, the era of high-interest yielding savings accounts is coming to an end. With effect from 1 May 2020, the 3 local banks will be revising the interest rates of their savings accounts, namely the DBS Multiplier, OCBC 360 and UOB One Account.

This article aims to provide an overview of the upcoming changes, how the existing account holders may be affected by the revision and to reveal which are the banks that still offer the best interest rate.

Revision of Interest Rates for DBS Multiplier Account

DBS Multiplier Account has underwent a major revamp recently in February which you may refer to in the previous post for more information.Starting from May, DBS will be reducing the interest rate for accounts that are only able to fulfill Income criteria as well as transaction in 1 additional category.

As shown in the table above, the interest rate for transaction amount in the range of $2,500 and $5,000 will be the most impacted with an absolute decline of 0.25% p.a. Unsurprisingly, most account holders probably fall within this transaction range for the crediting of their salary and credit card spending.

With this negative alteration, existing account holders would likely be incentivised to attain transactions in more categories besides Income. It should be noted that the interest rate for accounts that fall under Income + transaction in 2 or more categories is not affected in this upcoming revision. I have briefly discussed about some strategies that an account holder can employ to achieve transaction in 2 categories.

Revision of Interest Rates for OCBC 360 Account

Interestingly, there will be a slight increment to the Salary Bonus from 2% to 2.4% for account balance between $35,001 to $70,000. In addition, the barrier to earn Salary Bonus will be lowered from the salary crediting requirement of $2,000 to $1,800.

The credit card Spend Bonus and the Step-up Bonus (related to the increment of average daily balance) will be reduced to 0.2% and 0.4% for the first and next $35,000 respectively.

Based solely on these 3 bonus groups, the effective interest rate for $70,000 balance has reduced slightly from 2.5% to 2.4%. But of course, there is always the challenge of sustaining the Step-up Bonus.

In order to sustain the annual cycle, the account balance will be reset in Month 1. Thus, the Step-up Bonus for that month will be unqualified.

The interests are computed using the calculator available on the OCBC website which appears to have been updated with the revised interest rate.

Method 1

The account holder does not intend to have excess savings beyond $70,000 and therefore only maintain the maximum balance of $70,000 for which the bonus interest is accorded. He will not be able to earn the Step-up Bonus in this scenario. As calculated above, he will earn an effective interest rate of 2.15% and total interest of $1,534.

Method 2

The account holder starts with a balance of $64,500 and increases it by $500 per month. The effective interest rate that he is able to earn has jumped to 2.40% with the total interest calculated to be $1,641.

Method 3

Similar to Method 2, the account holder starts with a balance of $70,000 instead to maximise the interest earned. Subsequently, he increases the balance by $500 each month. The effective interest rate that he is able to earn is 2.34% with the total interest at $1,731.

Method 4

Beyond $70,000, the account holder has intended to recycle $500 only, which he faithfully deposits and withdraws on alternate months. The interest earned at $1,641 is still higher than that from Method 1.

To sum up the comparison, it would appear that Method 3 reaps the highest interest but falls marginally behind Method 2 in terms of effective interest rate.

One clean and simple way to gain the Step-up Bonus is to set a standing instruction to credit $500 on the first day of the month and transfer the $1,800 salary elsewhere on the day that it is credited. This is so as to maintain an average daily balance incremental amount of $500 every month.

Regardless, it would seem sensible to not overlook the significance of Step-up Bonus. This equates to an additional $200 interest that an account holder can earn in a year if he were to undertake Method 3 instead of Method 1.

Fortunately, the difference is meager when comparing the interest that one could potentially earn in the current and revised setting. As the increment to the Salary Bonus offsets the decline in Spend and Step-up Bonus, I would say that the upcoming revision to the OCBC 360 Account does not significantly impact the existing account holders.

On a side note, there are 2 other trivial adjustments to the Boost Bonus and Grow Bonus. The former awards extra interest on incremental balance amount whereas the latter only applies if the account balance is more than $200,000. As these 2 categories are not expected to have considerable influence on the interest earned for most account holders, I will not go into greater depth.

Revision of Interest Rates for UOB One Account

With the first $75,000 balance, an account holder is able to earn 2.44% but the interest rate will drop to 1.80% from May, a decline of 0.64%. The impact from the revision is the most severe at the first $60,000 balance in which the interest rate is reduced by 0.75%! Overall, the decrease across the account balance varies between 0.6% to 0.75%.

Overview of the Revision of Interest Rates for the 3 Local Banks

After plotting the revised interest rates trend lines for the 3 local banks in balance increment of $5,000, the peak interest rate for each savings accounts is more perceptible in the chart above.

For sizable balance amount above $50,000, OCBC 360 Account appears to dominate the local market at an attractive 2.45% interest rate. Taking into consideration the hurdle of sustaining the Step-up Bonus, the actual interest rate tends towards 2.4%. If we were to judge solely on the prerequisite of salary crediting, the OCBC 360 Account offers an enticing bonus interest rate of 1.8%.

Once the best savings account that offers 2.44% effective interest rate, the UOB One Account has certainly fallen from grace, paying out only 1.8% with this upcoming revision.

Despite recent revision, DBS Multiplier Account is still able to maintain its allure as a flexible savings account that mostly caters to lower account balance in the range of $25,000. Setting up a Regular Savings Plan can be a viable option to attain transactions in other categories and optimise the additional interest.

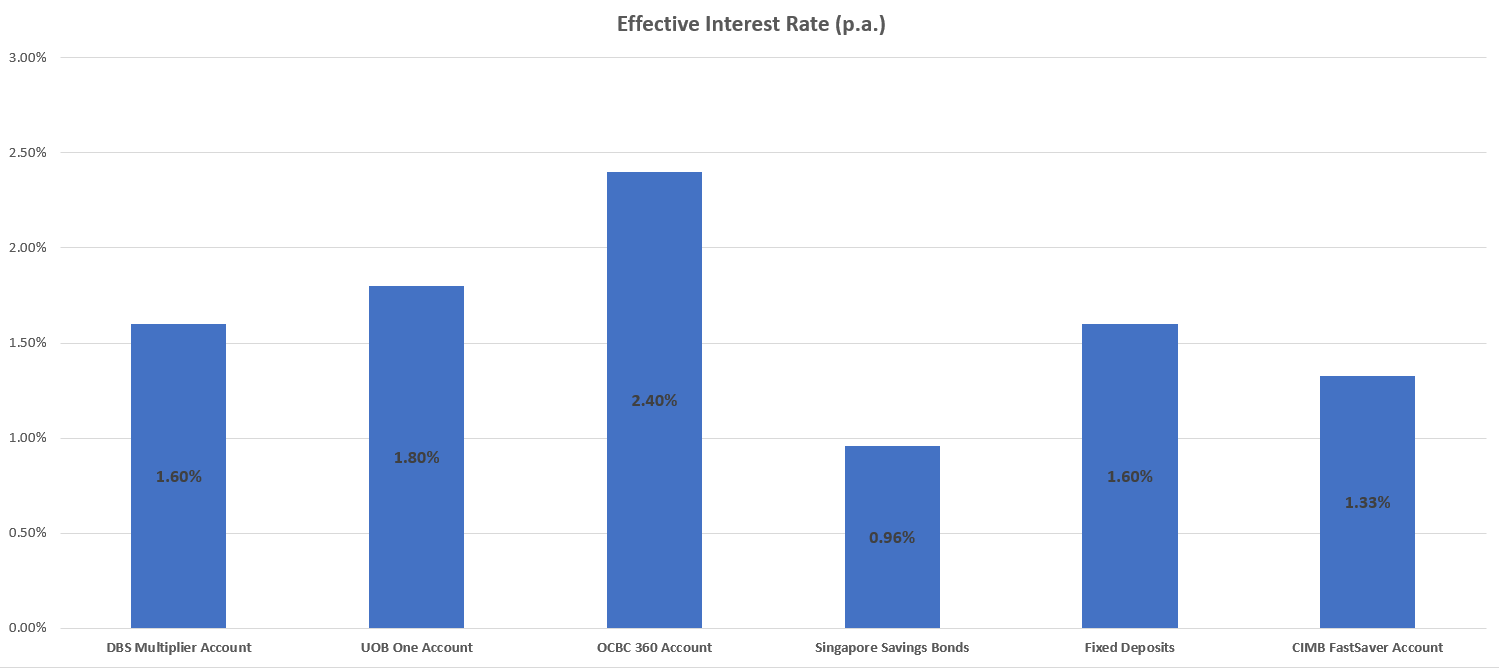

Comparison with other Active Savings Accounts

Comparison with other Savings Instruments

In the current environment of interest rate cuts, the interest rate reduction for savings accounts of the local banks seems to be in the region of that for other savings instruments.

- Singapore Savings Bonds: Using the data of the May 20 issue, the interest rates for Year 1 to 2 remain fairly constant at 0.96%. The minimum investment amount is $500 for each issue.

- Fixed Deposits: If you do not mind forgoing liquidity, UOB currently provides the highest interest rate of 1.60% on a 24-months fixed deposit with a minimum placement of $5,000. For a shorter period of 12 months, DBS is offering 1.4% with a minimum placement of $1,000.

- CIMB FastSaver Account: A fuss-free savings account that gives 1.325% on the first $100,000 balance.

If you do not wish to miss out on any articles, you may consider following the facebook page for timely update.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institutions and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

5 comments

Hi there,

ReplyDeleteYou have written a good and informative piece there.

I have a DBS multipier account and have been enjoying the high interest rates for a while. Do you know if the rates were also revised downwards for those with income plus three transactions?

My wife and I have a joint account where we credit in our monthly salaries and dividends, we have a home loan, credit card expenses plus we trade using the DBS Vickers trading platform. In all, our monthly transactions amount hit the $30,000 mark. Do you know if DBS had revised downwards the interest rate for this amount under the income plus three transactions? Last time it was still at 3.8%.

Looking forward to your reply.

Thank you!

Hi there,

DeleteTo the best of my knowledge, the upcoming revision in May will only impact the interest rate for Income + transactions in 1 category.

If you are able to hit $30,000 transaction amount and fulfill Income + transactions in 3 categories, you will still be able to earn 3.5% on the first $50,000 and 3.8% on the next $50,000.

Hello, First of all, thanks for sharing and appreciate your effort.

ReplyDeleteI myself finding way to optimise saving interest. I using OCBC 360 and I assumed if saving amount is over 70K, it's better to save as "Fixed Deposit" for more interest. May I know your opinion on that?

Looking forward to your reply.

Many Thanks!

Hi there,

DeleteIn my opinion, the Fixed Deposit currently offers reasonably competitive interest rate as compared to the other savings accounts in this present interest rate environment. The benefit is that you do not have to fulfill requirement on credit card spending or salary crediting. However, the money placed in FD will be relatively illiquid and you may not be able to touch them for a certain number of years (Taking the 1.6% on 24-months UOB fixed deposit as an example). So it is crucial to understand if you truly have no need for the use of this "excess" money as it would be a commitment to place them on FD.

Thanks for prompt reply and sharing your knowledge. Appreciated that!

Delete