Revision of Interest Rates for Standard Chartered Bonus$aver Account from 1 Apr 2020

By The Boy Who Procrastinates - March 21, 2020

First launched in Feb 2012, the Bonus$aver Account was one of the early trendsetters in active high-yielding savings accounts. It was extensively revamped in 2016 to gain competitive advantage among other financial institutions.

However, SCB will be revising the terms and conditions on the Bonus$aver Account for the second time with effect from 1 April 2020. You may also wish to refer to the circular for more information.

Revision of Interest Rates for Bonus$aver Account from 1 Apr 2020

- Credit Card Spend: The interest rate earned from monthly spending of $500 on the Bonus$aver card will be reduced from 0.78% to 0.45% p.a. Similarly, the interest rate for the next tier of $2,000 spending will be reduced from 1.78% to 1.45% p.a.

Unlike the UOB One Card, the Bonus$aver card itself offers no cashback/rewards/miles benefits and it has to be used with the savings account. And with SCB scaling back on the bonus interest, there is less incentive to spend on the Bonus$aver card.

Note that the figures might be different from what was advertised on the SCB website as I have excluded the prevailing interest rate for calculation.

- Bill Payments: The interest rate earned from the payment of 3 bills will be reduced from 0.25% to 0.1% p.a.

Another disheartening reduction of interest rate here. From 1 April, bonus interest rate of 0.1% p.a. would seem a pittance for account holders to go through the hassle of making 3 bill payment of at least $50, not to mention the various restriction that comes with it.

- Salary Crediting: The interest rate earned in this category will remain unchanged at 1% p.a.

- Invest/Insure: The interest rate earned in this category will increase from 0.75% to 1.28% p.a.

Based on the current t&c, it is required to purchase either a regular premium life insurance policy or invest in unit trust in order to fulfill this prerequisite. The bonus interest will only be paid for a consecutive period of 12 months.

Unlike DBS Multiplier Account, it would appear that SCB does not offer flexibility on the choice of products by specifically exclude investments via regular savings plans and exchange traded funds.

With that said, it may be unwise to acquire new life insurance plan or invest in unit trust for the sole purpose of achieving high interest on the savings account for 12 months. Personally, I would forgo this particular category.

- Prevailing Interest Rate: It will be reduced from 0.1% p.a. to 0.05% p.a.

Impact of Revision on the Interest Rate

The table above shows an overview of the revision to be made to the Bonus$aver Account from 1 April.

For an average account holder who credits his salary, pays 3 bills and spends $500 on his credit card, he will be receiving 1.6% interest rate on the Bonus$aver Account, an absolute decline of 0.53% from 2.13%.

For an average account holder who credits his salary, pays 3 bills and spends $500 on his credit card, he will be receiving 1.6% interest rate on the Bonus$aver Account, an absolute decline of 0.53% from 2.13%.

Undeniably, the Bonus$aver Account will lose its allure as a high-yielding savings account after the revision.

Comparison with other Active Savings Accounts

(Click to enlarge)

When set side by side with the other active savings accounts, the effective interest rate offered by the revised Standard Chartered Bonus$aver Account has lost its competitive edge and paled in comparison.

UOB One Account offers the best bang for the buck at 2.44% effective interest rate. This is followed closely by OCBC 360 Account at 2.43% but there is a need to sustain the cycle for Step-Up bonus.

The BOC SmartSaver also packs a punch at 2.35% effective interest rate, with an additional 0.60% p.a. extra bonus interest for balance above $60,000.

For the flexibility that it offers around the transaction amount in various categories, DBS Multiplier Account can also be considered, albeit at a lower bonus interest rate.

UOB One Account offers the best bang for the buck at 2.44% effective interest rate. This is followed closely by OCBC 360 Account at 2.43% but there is a need to sustain the cycle for Step-Up bonus.

The BOC SmartSaver also packs a punch at 2.35% effective interest rate, with an additional 0.60% p.a. extra bonus interest for balance above $60,000.

For the flexibility that it offers around the transaction amount in various categories, DBS Multiplier Account can also be considered, albeit at a lower bonus interest rate.

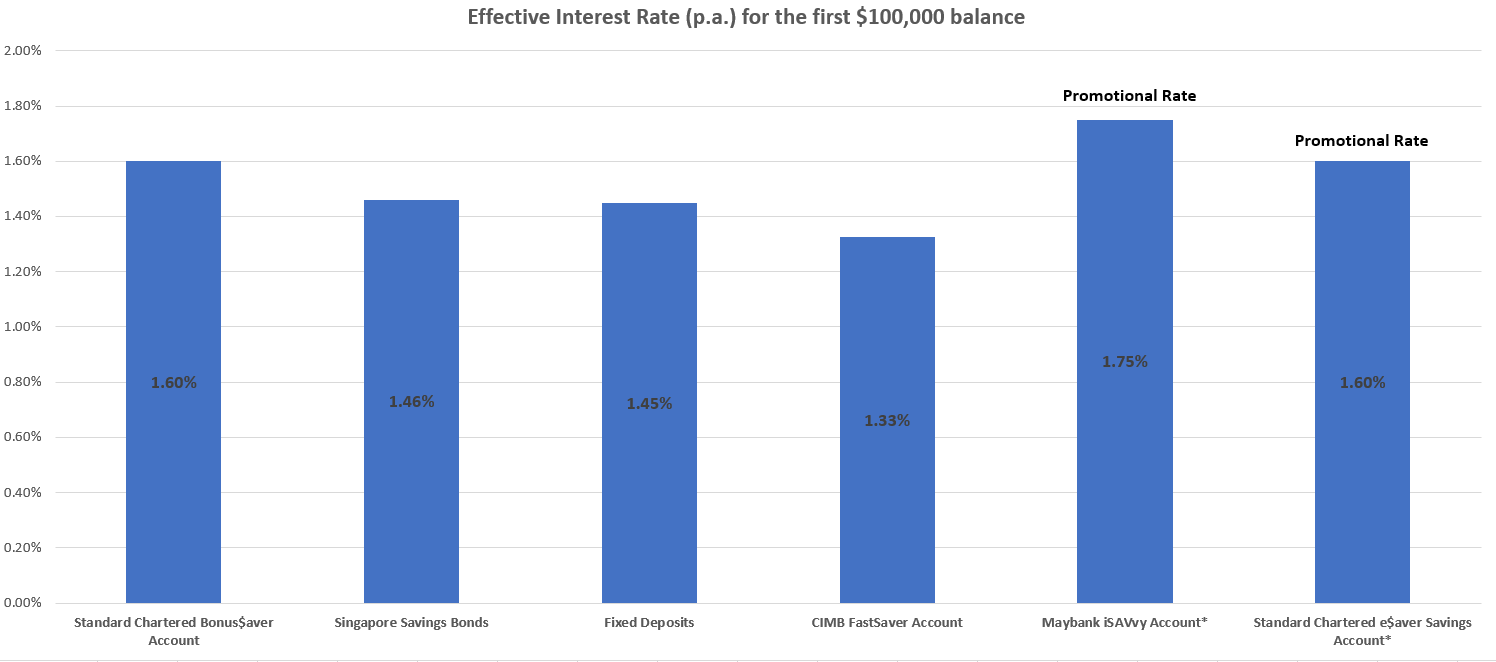

Comparison with other Savings Instruments

(Click to enlarge)

In the current environment of interest rate cuts, the reduction of interest rate for Bonus$aver Account seems to be in the region of that for other savings instruments.

- Singapore Savings Bonds: Using the data of the Apr 20 issue, the interest rates for Year 1 to 3 remain fairly constant at 1.46%. The minimum investment amount is $500 for each issue.

- Fixed Deposits: If you do not mind forgoing liquidity, Maybank currently provides the highest interest rate of 1.45% on a 12-months SGD time deposit with a minimum placement of $20,000.

- CIMB FastSaver Account: A fuss-free savings account that gives 1.325% on the first $100,000 balance.

- Promotional Interest Rate: Maybank iSAVvy Account offers a promotional rate of 1.75% on incremental balance until the end of April. As interest is credited on incremental balance, some may consider alternating funds with Standard Chartered e$aver Savings Account at 1.6% interest rate until the end of the month.

If you do not wish to miss out on any articles, you may consider following the facebook page for timely update.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institution and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institution and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

1 comments

https://saglamproxy.com

ReplyDeletemetin2 proxy

proxy satın al

knight online proxy

mobil proxy satın al

FJF4D