The thirtieth birthday is broadly considered to be a major milestone in many people's lives. In a sense, it marks the ultimate transition from the innocence of youth to the drudgery of adulthood.

Even though this milestone has crept up on Fitzgerald's narrator, Nick Carraway in The Great Gatsby, he speaks to the masses's unpopular view of turning thirty after having seen the wrong end of it.

I too turned 30 this month. While it is improbable that the path ahead will be that menacing, there is no reason that its commemoration cannot be portentous. Now on the cusp of adulthood, this will be a good opportunity to reflect on the past 3 decades.

Everyone has a story to tell. Everyone is a writer, some are written in the books and some are confined to hearts. And here's my journey thus far.

The Beginning

Staying in a humble 3-room HDB, I was raised in a family that extolled the virtues of prudent savings and frugality.

To a large extent, we could probably fit into the lower-middle income group. While making ends meet is not of grave concern, branded items in our household are rare, if not non-existent commodities.

With the family expenses focusing more on "needs" than "wants", we were mostly extricated from the materialistic expectations that the society has imposed upon us.

Looking back now, I wonder if some measures to scrimp and scrape were a little excessive. For instance, I would spend an hour walking to and from school daily in order to cut down on my transport cost. Educational excursions and involvement in extracurricular activities were scaled back. Visits to the malls and dining in restaurants were infrequent and entertainment for me came in the form of sports. Regardless, there is joy to be found with simple desires and living with less.

Even with paltry allowance, the national service is nevertheless an ideal period to squirrel away some savings, especially when it comes with food and lodging.

With the assistance of financial aid and the accumulation of savings through NS and part-time jobs during holidays, I am able to clear up the tuition fee debt fully like a Lannister. 😎

Even though the repayment of loan has depleted my savings, I do count myself lucky for not saddled with debts after graduation and able to commence the working phase with a clean slate.

Now, even with greater purchasing power, I still stay away from frivolous expense, maintaining a lifestyle of parsimonious thrift, relieved by occasional indulgence on travelling.

To a large extent, we could probably fit into the lower-middle income group. While making ends meet is not of grave concern, branded items in our household are rare, if not non-existent commodities.

With the family expenses focusing more on "needs" than "wants", we were mostly extricated from the materialistic expectations that the society has imposed upon us.

Looking back now, I wonder if some measures to scrimp and scrape were a little excessive. For instance, I would spend an hour walking to and from school daily in order to cut down on my transport cost. Educational excursions and involvement in extracurricular activities were scaled back. Visits to the malls and dining in restaurants were infrequent and entertainment for me came in the form of sports. Regardless, there is joy to be found with simple desires and living with less.

Even with paltry allowance, the national service is nevertheless an ideal period to squirrel away some savings, especially when it comes with food and lodging.

With the assistance of financial aid and the accumulation of savings through NS and part-time jobs during holidays, I am able to clear up the tuition fee debt fully like a Lannister. 😎

Even though the repayment of loan has depleted my savings, I do count myself lucky for not saddled with debts after graduation and able to commence the working phase with a clean slate.

Now, even with greater purchasing power, I still stay away from frivolous expense, maintaining a lifestyle of parsimonious thrift, relieved by occasional indulgence on travelling.

Significance of $100,000 as a milestone

Aside from being a nice, round number and one-tenth to becoming a millionaire, the importance of reaching this arbitrary $100,000 goal might be unfathomable to some.

Charlie Munger, the vice-chairman of Berkshire Hathaway and business partner of Warren Buffett, once uttered the following quote:

The first $100,000 is a bitch, but you gotta do it. I don't care what you have to do ⎯ if it means walking everywhere and not eating anything that wasn't purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.

The rationale is that $100,000 marks the threshold at which compound interest becomes significant with money working harder for you. Coupled with a consistent stream of savings/investment, it may produce a snowballing effect on the growth of net worth.

To illustrate this, we can consider the following scenario. Taking the median gross monthly income of Singaporeans at $4,437, the take-home pay is calculated to be approximately $3,034 after deducting CPF contributions.

Setting aside 30% of salary for investment, an individual is assumed to be able to faithfully invest approximately $10,000 every year, compounding at a rate of 5% per annum.

To illustrate this, we can consider the following scenario. Taking the median gross monthly income of Singaporeans at $4,437, the take-home pay is calculated to be approximately $3,034 after deducting CPF contributions.

Setting aside 30% of salary for investment, an individual is assumed to be able to faithfully invest approximately $10,000 every year, compounding at a rate of 5% per annum.

(Click to enlarge)

Now, we have a nice graph that depicts the journey to $1 million over the course of years. Reading from the chart, it takes 8.31 years to reach the first $100,000.

Interestingly, the gradient of the graph increases on the x-axis, indicating that the time taken to reach an additional $100,000 is exponentially shortened. At the other end of the spectrum, it takes just 1.78 years to get from $900,000 to a million dollar.

So, it does seem that the first $100,000 is indeed the hardest milestone to save up to. Beyond this threshold, the accumulation of wealth tends to be more attainable.

Interestingly, the gradient of the graph increases on the x-axis, indicating that the time taken to reach an additional $100,000 is exponentially shortened. At the other end of the spectrum, it takes just 1.78 years to get from $900,000 to a million dollar.

So, it does seem that the first $100,000 is indeed the hardest milestone to save up to. Beyond this threshold, the accumulation of wealth tends to be more attainable.

(Click to enlarge)

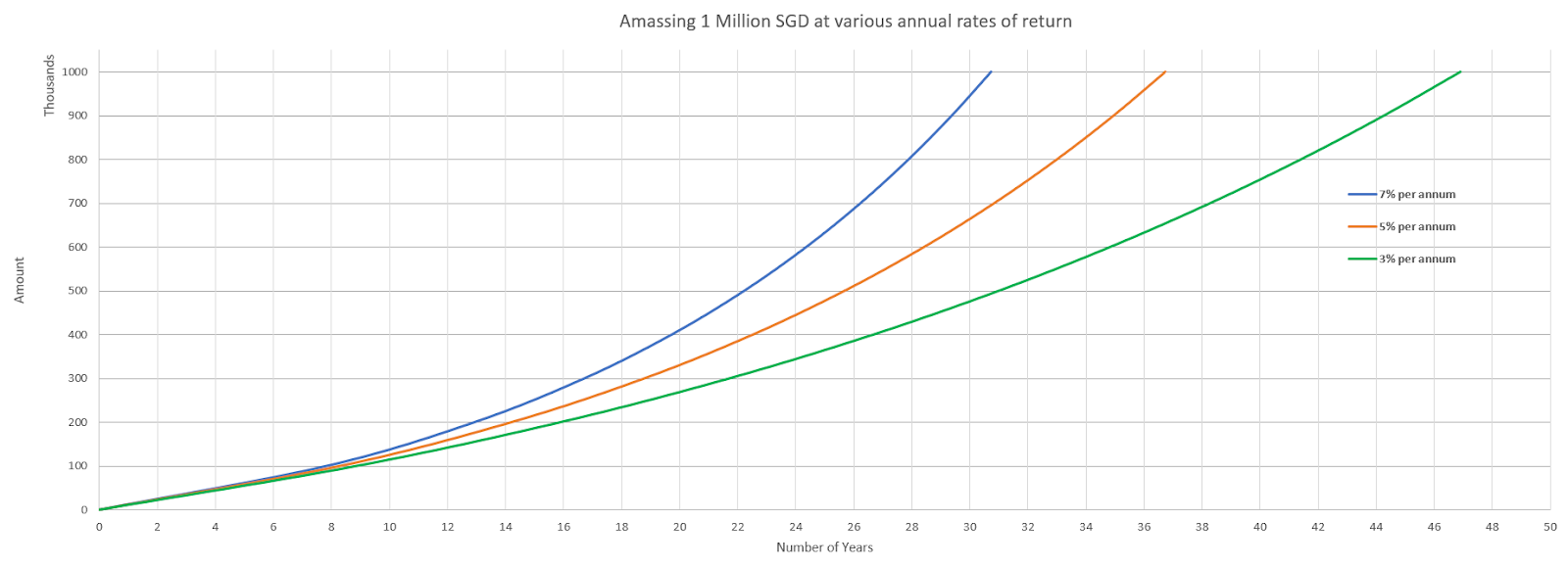

Plotting the graph over different annual rates of return does yield interesting observations.

Needless to say, the path to 1 million dollar is significantly shorter with greater rate of return (30.73 years at 7% returns against 46.90 years at 3% returns).

However, the difference in the number of years taken to amass the first $100,000 is almost indiscernible even when money is compounding at distinct rates of return. (7.84 years at 7% returns vs 8.88 years at 3% returns)

Therefore, it can be reasonably deduced that the rate of return does not have a pronounced impact in accelerating the time taken to reach the first $100,000.

Needless to say, the path to 1 million dollar is significantly shorter with greater rate of return (30.73 years at 7% returns against 46.90 years at 3% returns).

However, the difference in the number of years taken to amass the first $100,000 is almost indiscernible even when money is compounding at distinct rates of return. (7.84 years at 7% returns vs 8.88 years at 3% returns)

Therefore, it can be reasonably deduced that the rate of return does not have a pronounced impact in accelerating the time taken to reach the first $100,000.

How to save $100,000

As illustrated in the graphs above, there is no shortcut to save up to your first $100,000 and it all comes down to a brute force solution of diligent saving.My portfolio has crossed the $100,000 mark towards the end of 2018. However, the net profits from closed positions and dividend collected takes up a mere 9.72% of it.

Admittedly, it is easier to save up at this stage without the additional expense of starting a family yet. In any case, here are some of the measures I have taken to attain this seemingly lofty goal:

- Scout around and choose a savings account that yields the high interest rate. Every extra penny counts towards reducing the monthly expense.

- Keep track of your monthly cash inflow and outflow. This provides a clearer picture of what your money was mostly spent on. Once the monthly expense has been classified into the categories of "wants" and "needs", it is easier to be disciplined in managing your finance.

- Be smart with your spending and set the right priorities. Cut down on frivolous and unnecessary expenses ranging from branded goods to expensive cab rides everyday. For example, consider whether the need to take cab/purchase a car is justifiable when there is public transportation available as cheaper substitute.

Before embarking on my career, I have been using the same POSB savings account with 0.05% interest rate and have not placed any fixed deposit or carried out bank transfer before. Because of that, starting a financial blog has initially been more of a pipe dream for me.

However, everything is possible if we put every effort on what we strive for. Similarly, with sheer determination, sensible budgeting and mindful spending, it is definitely achievable to reach this milestone even if we were not born with silver spoons in our mouths.

Two roads diverged in a wood, and I ⎯

I took the one less traveled by,

And that has made all the difference.

⎯ Robert Frost

4 comments

Hi there, I applaud you on achieving your first $100,000. Living frugally and within your means are good habits to inculcate and maintain. But extreme (or excessive as you put it) frugality isnt the way to go. Having worked more than 30 years, and saved enough for a comfortable retirement (where our passive income covers our expenses with a comfortable margin), let me share the following points :

ReplyDelete1. To build up meaningful weatlh, savings alone is not going to do it. You need to go out and earn more! For eg., if you earn $3,000 a month and save 100% of it, you will only save $36,000 a year. On the other hand, if you earn $10,000 a month, and save 50% of it, you will have $60,000 saved a year and still have a life! My point is, life is to be lived and not wasted away living like a hermit in a spartan condition.

2. Compounding interest is alluring. The higher the interests, the more attractive the concept of compounding interest. You should know, your beautiful charts showed the returns but thats in theory. In reality, where is one going to find an investment that will give you a good (and risk free) and consistent return over 20, 30 or more years!? What I found so far is that only the CPF can give such consistent returns over many years (with almost zero risk) albeit with 2.5% (OA) and 4% (SA, MA and RA - for those 55 yo and above). My wife and I have been beefing up our CPF to take advantage of this, so much so that we are receiving substantial yearly interest from CPF. Our CPF interest is now our anchor (highest) passive income source, and augmented by our dividend income (second highest, more than $5,000 per month) and rental income (lowest)

3. Youth (and thus time) is an important factor in building up wealth. Be patient and dont be greedy. Some investments just need time to "blossom".

All the best in your wealth building journey.

Hi there,

DeleteThat's really great advice. Thanks for sharing! 🙂

Please join Us to find out how you can achieve financial independence. ,

ReplyDeleteThanks for sharing the blog, seems to be interesting and informative too. Can you suggest some of the interesting places to visit for best insurance in singapore

ReplyDelete