Topping up MediSave to enjoy Tax Relief and Free Medical Insurance Coverage

By The Boy Who Procrastinates - June 15, 2019

Following the previous article on Unlocking the Potential of CPF, I have made a voluntary cash contribution to my Medisave Account (MA).

The primary intention is to optimise the additional 1% interest earned on the first $60,000 combined CPF accounts. Personally, I find it difficult to pass on the extra interest which would make a significant difference under the compounding effect over the span of 25 years.

The primary intention is to optimise the additional 1% interest earned on the first $60,000 combined CPF accounts. Personally, I find it difficult to pass on the extra interest which would make a significant difference under the compounding effect over the span of 25 years.

Voluntarily contributing to MA also allows me to claim tax relief for YA 2020 (ie. income earned in 2019). Furthermore, the increased interest generated by the growing MA balance helps to provide "free" medical insurance coverage payable by Medisave.

As we know, nothing good is ever completely one-sided. Despite the multiple advantages as outlined above, one should be mindful of the illiquidity aspect of CPF funds as a main trade-off of the top-up.

Tax Relief

According to IRAS, a taxpayer is allowed to claim tax relief for voluntary Medisave contributions.The amount of tax relief, is however subjected to the annual CPF contribution cap and the Prevailing Basic Healthcare Sum. Additionally, the total amount of personal income tax relief is subjected to an overall relief cap of $80,000 per year of assessment.

Annual CPF contribution cap

It refers to the maximum amount of mandatory and voluntary contributions to all 3 CPF Accounts that a CPF member can receive in a calendar year. That includes the 20% compulsory CPF contribution as an employee and 17% compulsory CPF contribution by the employer.

Currently, the CPF Annual limit is set at $37,740.

Basic Healthcare Sum (BHS)

The BHS refers to the maximum amount that one can have in his MA. It is adjusted yearly but once an individual turns 65, the BHS will be fixed for life.

The prevailing BHS for CPF members aged 65 and below in 2019 is $57,200.

Compared to the other CPF accounts, MA has a lower ceiling which makes it relatively achievable to reach the maximum balance. Once your MA has reached the BHS, any excess contribution will flow to your Special Account (SA), or Ordinary Account (OA) if SA has reached the prevailing Full Retirement Sum (FRS).

Source: CPF website

Usage of Medisave

Being a national medical savings scheme, Medisave can be used for various healthcare related expenses.

Commonly, it can be used to pay for the premiums of MediShield Life, Integrated Shield Plans (ISP) and ElderShield, as well as the mandatory CareShield Life from 2020 onwards.

On top of that, it can be used for vaccinations, pregnancy and delivery expenses, as well as other general inpatient and outpatient care and long-term rehabilitative care, subjected to a certain limit. The use of Medisave can also be extended to immediate family members such as spouse, children, parents and grandparents.

Compared to SA which caters mainly for CPF Investment Scheme, I personally find that topping up to MA offers a more versatile option.

Commonly, it can be used to pay for the premiums of MediShield Life, Integrated Shield Plans (ISP) and ElderShield, as well as the mandatory CareShield Life from 2020 onwards.

On top of that, it can be used for vaccinations, pregnancy and delivery expenses, as well as other general inpatient and outpatient care and long-term rehabilitative care, subjected to a certain limit. The use of Medisave can also be extended to immediate family members such as spouse, children, parents and grandparents.

Compared to SA which caters mainly for CPF Investment Scheme, I personally find that topping up to MA offers a more versatile option.

"Free" Medical Insurance Coverage

With the funds in MA generating 4% interest rate annually, the additional interest may be sufficient to cover the premium of ISP. Looking at it from another perspective, the CPF interest credited can effectively be used to provide "free" medical insurance coverage.

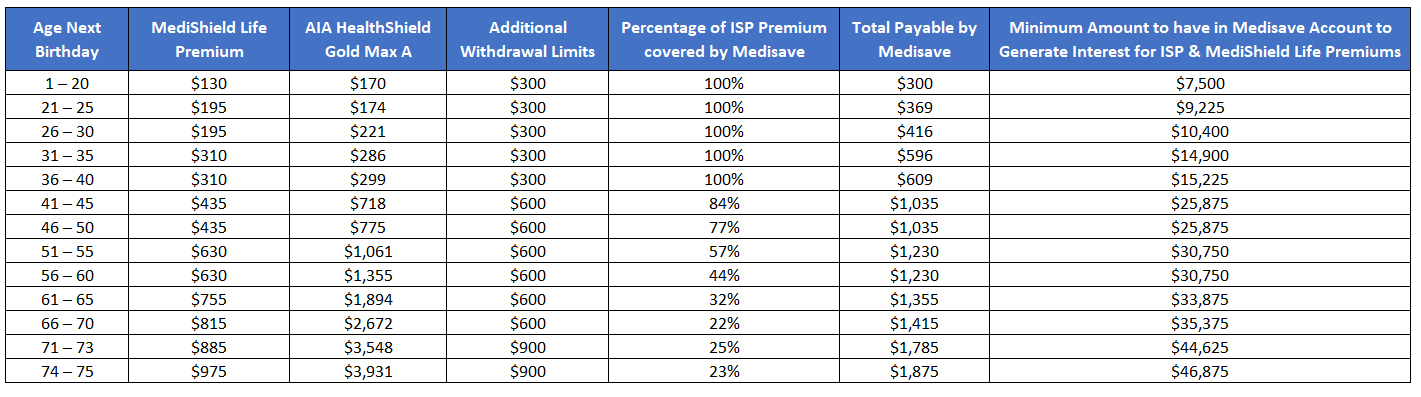

However, the amount of Medisave that an individual is able to pay for the premium of ISP is subjected to the Additional Withdrawal Limits (AWL).

To illustrate this, let's take a look at one of the private hospital plans, AIA HealthShield Gold Max A for example.

However, the amount of Medisave that an individual is able to pay for the premium of ISP is subjected to the Additional Withdrawal Limits (AWL).

To illustrate this, let's take a look at one of the private hospital plans, AIA HealthShield Gold Max A for example.

Source: AIA Brochure

According to the tabulation above, an individual reaching the age of 30 will be paying $195 for MediShield Life and $221 for ISP separately. As the AWL of $300 is higher than the ISP premium, the total premium can be paid for using Medisave, with no cash outlay.

Now, if he has at least $10,400 balance in his MA, the 4% interest generated is sufficient to pay for the premiums of both MediShield Life and ISP. In such scenario, the payment of the insurance coverage premium does not eat into his original MA balance.

Do note that the calculation does not include the premium of riders as they are not payable by Medisave.

How to do a Voluntary Cash Contribution to Medisave Account

If you are keen in doing a voluntary cash contribution to your MA, you can do so via CPF Portal.

Source: CPF Website

Once you are logged on to the CPF Portal, you may navigate to "My Requests" page using the side bar on the left. Subsequently, the cash contribution page can be found under the "Building up My CPF savings" header as shown in the diagram above.

Another thing to take note of is that CPF interest is calculated based on the lowest balance of the month. Therefore, it would probably be logical to make a voluntary contribution closer to the end of the month.

Closing Thoughts

Given the ample time available until retirement, it would make sense to ride on the compounding effect and optimise the additional interest as early as possible. Topping up Medisave also offer a more flexible option for covering healthcare related expense in future.

However, I recognise that the choice to voluntarily contribute to Medisave may be less favourable for those who prefer or in need of cash flow. It is thus crucial to strike a balance between enjoying the benefit of voluntary contribution to CPF and the liquidity of cash.

If you do not wish to miss out on any articles, you may consider following the facebook page for timely update.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with CPF Board and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

3 comments

Thank you for sharing such great information.

ReplyDeleteIt has help me in finding out more detail aboutmedical insurance coverage

ReplyDeleteI came across this link on investment linked policy, hope can provide more insights.

investment linked policy

Thank You for sharing such a wonderful blog, it is very useful. Best Life Insurance In Singapore

ReplyDelete