Increment of Salary Bonus for OCBC 360 Account from 1 April 2019

By The Boy Who Procrastinates - April 13, 2019

It was subsequently confirmed that this favourable news is here to stay and is now a permanent feature of the OCBC 360 account until further notice. With that, this article aims to find out the additional amount of interest an account holder can expect to earn, as well as to compare across different methods to fully utilise the step-up bonus. You may wish to refer to the OCBC website for more information.

Revision of Interest Rate for OCBC 360 from 1 April

From 1 April, the Salary Bonus interest for balances between $35,000 and $70,000 has been increased from 1.5% to 2% per year.

Account holders can still earn 1.2% interest on the first $35,000 and the minimum salary crediting amount has remained unaltered at $2,000.

On the whole, the effective interest rate on $70,000 balance contributed by the category of Salary Bonus has raised from 1.35% to 1.6%.

Impact of the Revision on the Interest Rate

(Click to enlarge)

For ease of comparison, let's consider the scenario in which the salary, spend and step-up bonus of OCBC 360 Account are fulfilled.

Graphically, we can observe that the revision provides a significant interest rate increment beyond $35,000 balance. At the maximum account balance of $70,000, the account holder can earn an effective interest rate of 2.55%, translating to a gain of 0.25% or $175 per year.

Graphically, we can observe that the revision provides a significant interest rate increment beyond $35,000 balance. At the maximum account balance of $70,000, the account holder can earn an effective interest rate of 2.55%, translating to a gain of 0.25% or $175 per year.

(Click to enlarge)

Of course one might argue that the maintenance of step-up bonus can be demanding and some would prefer the flexibility of channelling the excess funds for better use.

If the salary credited was promptly transferred out of the savings account, the step-up bonus would be unaccomplished. In such situation, the revised effective rate can reach 2.1% instead of the current 1.85% at $70,000 balance, an absolute gain of 0.25%.

As this amendment only affects the second balance tier, it would only benefit account holders who have parked more than $35,000 in their accounts.

If the salary credited was promptly transferred out of the savings account, the step-up bonus would be unaccomplished. In such situation, the revised effective rate can reach 2.1% instead of the current 1.85% at $70,000 balance, an absolute gain of 0.25%.

As this amendment only affects the second balance tier, it would only benefit account holders who have parked more than $35,000 in their accounts.

Ways to Optimise the Step-up Bonus

In the previous post regarding the revision of interest rate for OCBC 360 Account, I have examined a hack to perpetuate the step-up bonus chiefly by utilising the mechanism of daily average balance ("ADB"). However, I understand that such method may not be as sustainable as expected due to the increasing sum to deposit in the account.

To remove the complexities from the equation, we can narrow down to the few approaches illustrated in the table below.

For ease of comparison, we assume the profile of an account holder who is able to fulfill the salary and spend bonus. To simplify the calculation for step-up bonus, he can choose to deposit $500 at the start of the month and transfer out his salary credited within the same day. This will help to maintain an incremental ADB of $500 that is easier to keep track of.

(Click to enlarge)

In order to sustain the annual cycle, the account balance will be reset in Month 1. Thus, the step-up bonus for that month will be unqualified.

The interests are computed using the calculator available on the OCBC website.

Method 1

The account holder does not intend to have excess savings beyond $70,000 and therefore only maintain the maximum balance of $70,000 for which the bonus interest is accorded.

As calculated above, he will earn an effective interest rate of 2.10% and total interest of $1,498.

Method 2

The account holder starts with a balance of $64,500 and increases it by $500 per month. The effective interest rate that he is able to earn has jumped to 2.49% with the total interest calculated to be $1,708.57.

Method 3

Similar to Method 2, the account holder starts with a balance of $70,000 instead to maximise the interest earned. Subsequently, he increases the balance by $500 each month.

The effective interest rate that he is able to earn is 2.43% with the total interest at $1,798.33.

Method 4

Beyond $70,000, the account holder has intended to recycle $500 only, which he faithfully deposits and withdraws on alternate months. The interest earned at $1,661.22 is still higher than that from Method 1.

To sum up the comparison, it would appear that Method 3 reaps the highest interest but falls marginally behind Method 2 in terms of effective interest rate.

Regardless, it would seem sensible to not overlook the significance of step-up bonus. This equates to an additional $300 interest that an account holder can earn in a year if he were to employ Method 3 instead of Method 1.

Comparison with other Active Savings Accounts

Following from the previous post on the comparison among the active savings accounts, let's see where OCBC 360 account stands with the latest revision to its salary bonus.

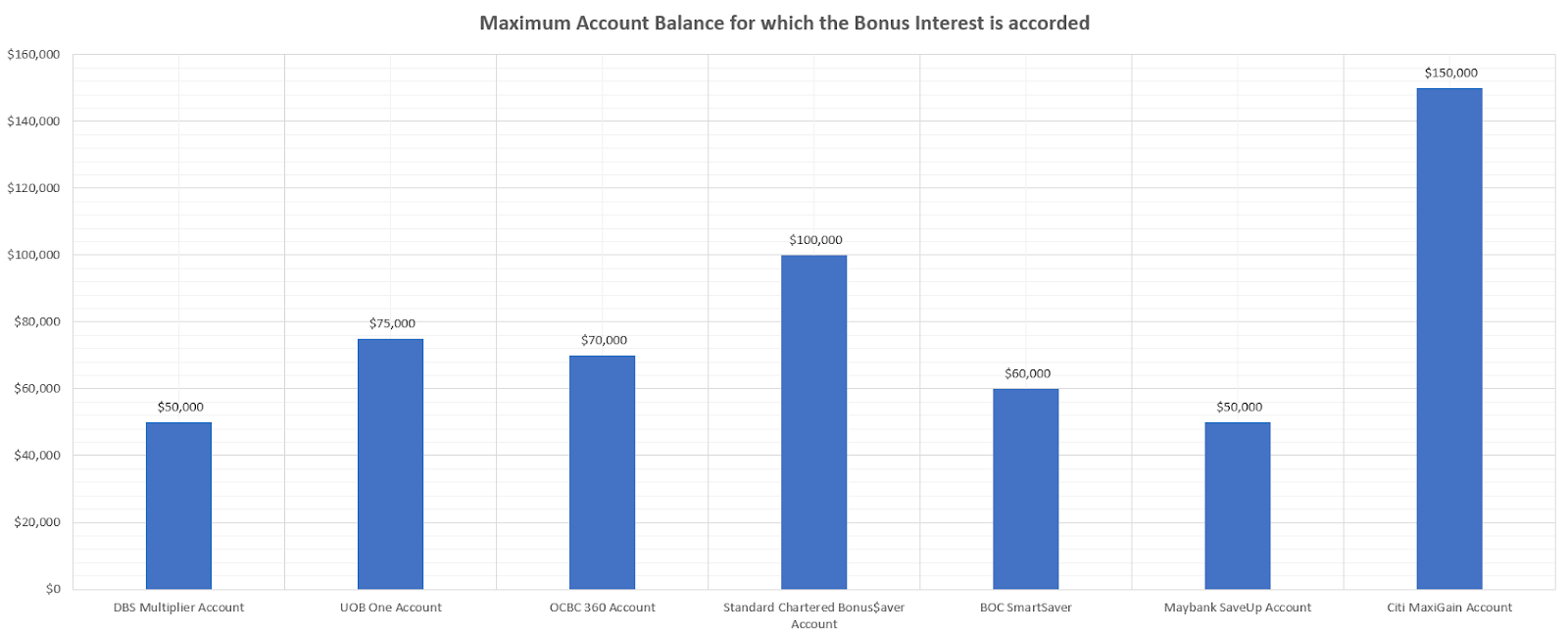

As a disclaimer, I have cheated a little and included Citi MaxiGain Account as one of the contenders. This is because the MaxiGain account offers competitive interest rate which rivals that of the other active savings accounts despite being a passive savings account.

With the addition of a new candidate, the OCBC 360 Account has been shifted to 4th placing in terms of maximum balance for which the bonus interest is accorded. The Citi MaxiGain Account leads the pack at $150,000, followed by Standard Chartered Bonus$aver Account ($100,000) and UOB One Account ($75,000).

According to the ABS website, the 1-Month SIBOR is currently at 1.82283. Therefore, the Citi MaxiGain Account currently offers the best bang for the buck at 2.48% with a few caveats such as the building up of 12 counters (represented by the orange bar) and a balance of at least $70,000. Additionally, its effective interest rate is subjected to the fluctuation of SIBOR.

For the sake of comparison, the Method 3 depicted above is being used as a benchmark for the computation of effective interest rate for OCBC 360 Account. With the boost from the salary bonus increment, the OCBC 360 Account has sharpened its competitive edge and is now almost on par with UOB One Account.

If we were to judge solely on the prerequisite of salary crediting of at least $2,500, the OCBC 360 offers the 2nd highest interest rate at 1.6%, behind DBS Multiplier at 1.85% (considering the credit card spending of $1 to be negligible).

As a disclaimer, I have cheated a little and included Citi MaxiGain Account as one of the contenders. This is because the MaxiGain account offers competitive interest rate which rivals that of the other active savings accounts despite being a passive savings account.

(Click to enlarge)

With the addition of a new candidate, the OCBC 360 Account has been shifted to 4th placing in terms of maximum balance for which the bonus interest is accorded. The Citi MaxiGain Account leads the pack at $150,000, followed by Standard Chartered Bonus$aver Account ($100,000) and UOB One Account ($75,000).

(Click to enlarge)

According to the ABS website, the 1-Month SIBOR is currently at 1.82283. Therefore, the Citi MaxiGain Account currently offers the best bang for the buck at 2.48% with a few caveats such as the building up of 12 counters (represented by the orange bar) and a balance of at least $70,000. Additionally, its effective interest rate is subjected to the fluctuation of SIBOR.

For the sake of comparison, the Method 3 depicted above is being used as a benchmark for the computation of effective interest rate for OCBC 360 Account. With the boost from the salary bonus increment, the OCBC 360 Account has sharpened its competitive edge and is now almost on par with UOB One Account.

If we were to judge solely on the prerequisite of salary crediting of at least $2,500, the OCBC 360 offers the 2nd highest interest rate at 1.6%, behind DBS Multiplier at 1.85% (considering the credit card spending of $1 to be negligible).

(Click to enlarge)

Merging the information from the first 2 charts, we can measure the maximum bonus interest that one can potentially earn from these savings accounts.

Needless to say, Citi MaxiGain Account and the Standard Chartered Bonus$aver Account have clinched the first 2 positions, attributed to their impressively high cap on the balance that earns the additional interest.

The UOB One Account still has a slight advantage over OCBC 360 Account due to its marginally higher balance cap of $75,000.

Although it is still far from its generous 3.05% interest rate back in 2014, I must say OCBC has made a decent move in closing on the gap among its peers.

Disclaimer: Kindly note that this is not a sponsored post. The author is in no way affiliated with the stated financial institution and does not receive any form of remuneration for this post. The Boy who Procrastinates has compiled the information for his own reference, with the hope that it will benefit others as well.

2 comments

still lost to UOB and DBS <$45K

ReplyDeleteHi Layers!

DeleteYes, as you have rightly pointed out, the interest rate earned also depends on the amount of bank balance that one has at his disposal.